Daily Market Outlook - Friday, March 28

Image Source: Pexels

Asian stocks fell on Friday, with sharp declines in South Korea and Japan as safe-haven gold surged to an all-time high. The sell-off followed the announcement of new tariffs by U.S. President Donald Trump, escalating fears of a potential trade war among investors. Trump unveiled a 25% tariff on auto imports set to take effect next week, sparking widespread criticism from global politicians and industry leaders. Automakers worldwide warned of looming price hikes as a result of the tariffs. The escalating trade tensions, initiated by Trump after his election, have rattled financial markets, particularly weighing on the shares of international automakers. In Asia, Japan’s Nikkei index tumbled over 2%, led by steep losses in Toyota and Honda stocks. South Korea’s benchmark index dropped 1.3% to a two-week low, as the automotive sector remains vital to both nations' economies. In contrast, Hong Kong’s Hang Seng index gained 0.6%, largely unaffected by the auto tariff concerns. Trump hinted at the possibility of reducing tariffs on China to finalise a deal with ByteDance, the Chinese parent company of TikTok, regarding the app's sale.

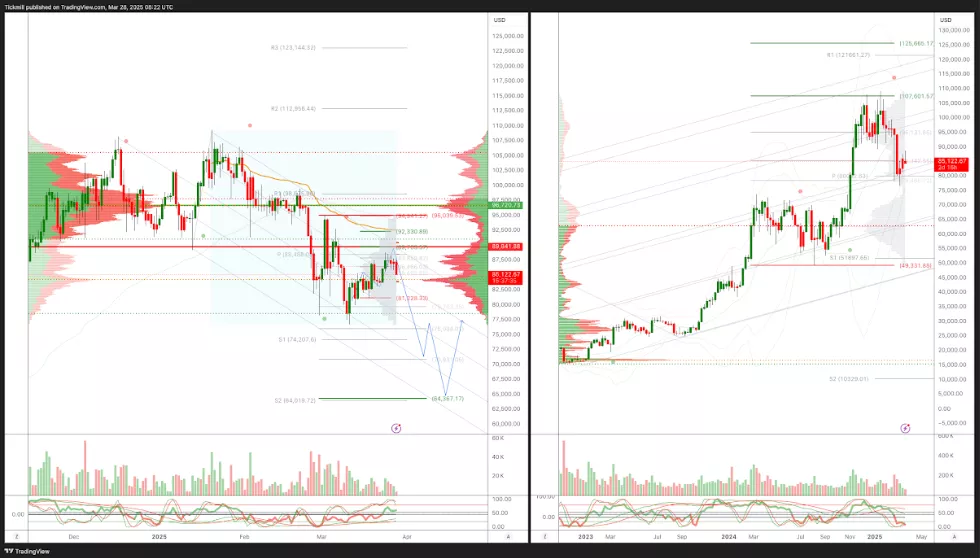

Most major car manufacturers are grappling with an uncertain future, but not all share the same challenges. Texas-based electric vehicle giant Tesla stands out, with its stock largely unaffected by these concerns. Unlike many competitors, Tesla’s U.S. production heavily relies on domestic facilities and significantly fewer foreign-made components. Investor attention is now turning to the anticipated U.S. tariffs set to be announced next week. Markets have reacted to President Trump’s suggestion that the tariffs might be mild, but the situation remains unpredictable, leaving room for both positive and negative surprises. Amid this climate of uncertainty, gold prices continue their upward trajectory, recently hitting another all-time high as investors seek safe-haven assets. Since breaking the $3,000 per ounce threshold in mid-March, gold has stayed comfortably above that mark. The precious metal has surged over 17% during the January-March quarter, positioning itself for its strongest quarterly performance since 1986.

In the UK the ONS maintained its Q4 2024 GDP estimate at +0.1% q/q, as expected, with annual growth revised up to 1.1% from 0.9%, though per capita growth remains flat at 0.0%. Market sector GDP underperformance, noted by the BoE, persists. The household savings ratio rose to 12.0% from 10.3%, signalling cautious consumer sentiment. Despite stronger-than-expected February retail sales (+2.2% y/y core growth), the results may partly reflect January revisions and a dip in the price deflator. The easing deflator (1.4% to 1.0% y/y) boosts reported volumes but could be temporary. The data doesn't significantly impact short-term policy discussions.

Next week is shaping up to be pivotal, particularly from a U.S. perspective, with significant attention on tariff announcements and implementation scheduled for Wednesday and Thursday. February trade data, due Thursday, will provide additional insights into the early effects of existing tariffs. Trade policy uncertainty has already weighed on expectations, with the consensus for Tuesday’s manufacturing ISM forecast dipping below 50. Adding to the week’s importance, the monthly labour market report will be released, and Federal Reserve Chair Powell is set to address these developments on Friday.

In the eurozone, the key focus will be on flash March inflation data on Tuesday, following Germany’s inflation figures on Monday. European Central Bank (ECB) President Christine Lagarde is also expected to speak at an AI conference on Tuesday, while the minutes from the March ECB meeting will be released on Thursday.

In the UK, attention will centre on comments from the Bank of England’s Greene on Tuesday, which are likely to include terms such as "gradual," "cautious," and "careful." Key survey data, including the Lloyds Business Barometer (Monday) and the BoE Decision Maker Panel (Thursday), are also on the agenda. However, it could be a quieter week overall for the UK. Elsewhere, Japan’s Tankan survey is due Monday, the Reserve Bank of Australia will announce its rate decision on Tuesday, and final March PMIs will be released globally on Monday and Wednesday.

Overnight Newswire Updates of Note

- PM Carney: Nothing Off Table As Canada Plans Tariff Retaliation

- Slovak Premier’s Attempt To Replace ECB's Kazimir Falters

- EU Set To Limit Apple And Meta Fines To Avoid Ire Of Donald Trump

- European Leaders Reject Russian Demands For Sanctions Relief

- US Seeks To Control Ukraine Investment, Squeezing Out Europe

- Elon Musk: DOGE Aims To Finish $1T In Cuts By End Of May

- Porsche, Mercedes Face Biggest Tariff Hit; Ferrari Raises Prices

- Japan PM Expects ‘Big’ Economic Impact From Trump Car Tariffs

- Tokyo Consumer Inflation Picked Up In March On Higher Food Prices

- BoJ Policy Board Has Grown More Cautious Of US Policy Risks

- China’s Xi Urges World Business Leaders To Protect Global Trade

- Goldman Scraps April RBA Cut, Still Sees Meeting As ‘Close Call’

- Aussie PM Albanese Calls May 3 Election As Polls Show Close-Race

- Gold Hits Record High As US Tariffs Spark Trade Tensions

- NYSE Halts GameStop Shorts As BTC Bet Triggers Plunge

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0750 (1.5BLN), 1.0800 (2.9BLN), 1.1000 (570M), 1.1025 (1BLN)

- USD/CHF: 0.8790 (352M). GBP/USD: 1.2825 (236M)

- EUR/CHF: 0.9550 (695M), 0.9600 (700M), 0.9650 (680M)

- EUR/GBP: 0.8300 (575M), 0.8350-60 (652M), 0.8400 (454M), 0.8450 (804M)

- AUD/USD: 0.6380 (354M)

- USD/CAD: 1.4145 (1BLN), 1.4230 (250M), 1.4300 (365M), 1.4330-40 (914M)

- USD/JPY: 149.00 (351M), 149.25-30 (667M), 150.00 (301M), 150.40 (920M

- 151.00 (1.4BLN), 153.00 (984M)

Banks are now issuing signals for FX hedge rebalancing at the end of the month and quarter. Models indicate a strong demand for the USD in both scenarios. The Barclays model highlights significant demand for the USD against all major currencies at month-end. Conversely, the quarter-end model, which utilizes the same methodology, reflects a moderate signal against all major currencies. Nonetheless, this model also forecasts a robust demand for the USD compared to the EUR. It's worth noting that short-term expiry FX options have been set up for potential setbacks in the EUR/USD.

CFTC Data As Of 21/3/25

- In the foreign exchange markets speculative traders have adopted a bearish stance on the US dollar. The euro holds a net long position of 59,425 contracts, while the Japanese yen leads with a net long position of 122,964 contracts. In contrast, the Swiss franc shows a net short position of -34,375 contracts, and the British pound maintains a net long position of 29,402 contracts. Bitcoin's net long position is modest at 1,841 contracts.

- In the bond market, speculators have reduced the net short position for CBOT US Treasury bond futures by 20,694 contracts, bringing it down to 13,510. Similarly, the net short position for CBOT US Ultrabond Treasury futures has decreased by 4,236 contracts to a total of 247,158. For CBOT US 2-Year Treasury futures, the net short position has been trimmed by 1,659 contracts, now standing at 1,220,556. However, the net short position for CBOT US 10-Year Treasury futures surged by 144,299 contracts to reach 881,374, while CBOT US 5-Year Treasury futures saw an increase of 32,573 contracts, totaling 1,905,940.

- In the equities market, equity fund managers reduced their net long position in the S&P 500 CME by 9,572 contracts, bringing it to 832,269. Meanwhile, equity fund speculators cut their net short position by 9,127 contracts, now totaling 195,491.

Technical & Trade Views

SP500 Pivot 5790

- Daily VWAP bearish

- Weekly VWAP bearish

- Seasonality suggests bullishness into late April

- Above 5885 target 5950

- Below 5815 target 5415

(Click on image to enlarge)

EURUSD Pivot 1.0750

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into March 30th

- Above 1.0750 target 1.11

- Below 1.0690 target 1.0550

(Click on image to enlarge)

GBPUSD Pivot 1.28

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 1.2850 target 1.32

- Below 1.2790 target 1.2660

(Click on image to enlarge)

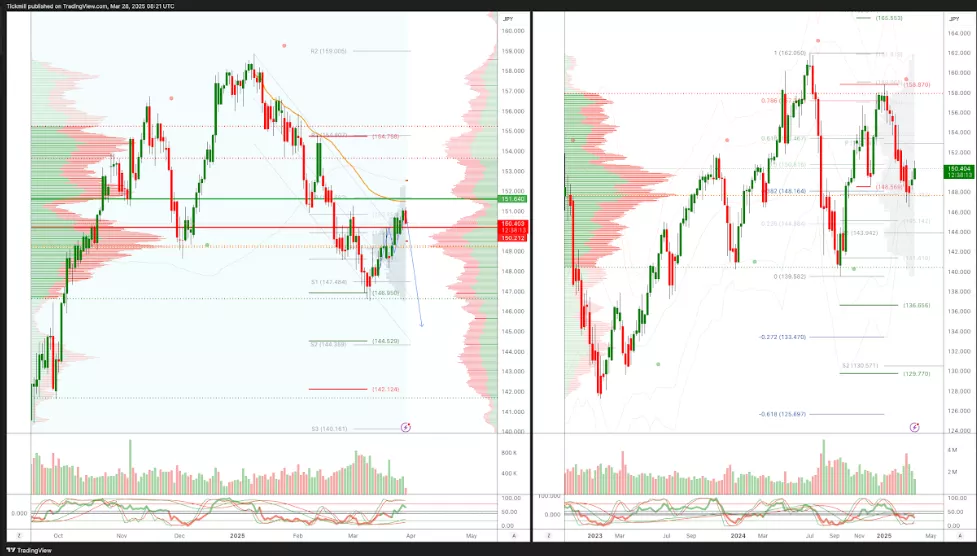

USDJPY Pivot 150.50

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into Apr 9th

- Above 1.52 target 153.80

- Below 150.50 target 145

(Click on image to enlarge)

XAUUSD Pivot 2950

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into mid/late March

- Above 2900 target 3100

- Below 2880 target 2835

(Click on image to enlarge)

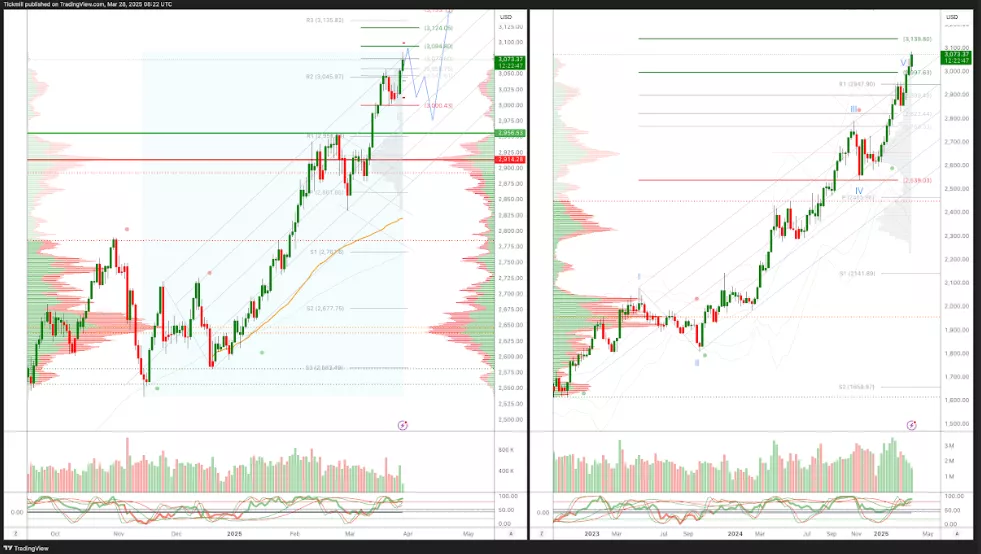

BTCUSD Pivot 90k

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 97k target 105k

- Below 95k target 65k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Thursday, March 27

Daily Market Outlook - Thursday, March 27

The FTSE Finish Line - Wednesday, March 26